If you’re contemplating buying a home – the topic of financing has likely come up. Unless you plan to purchase with cash, you’ll need to understand applying for a mortgage. According to the National Association of Realtors 2022 Profile of Home Buyers and Sellers, 97% of first time home buyers financed their home purchase and 78% financed their home. Pre-approval is one of the first steps in buying a home. It will show sellers you are serious, have done some homework an you’ll be prepared to make an offer when the time is right. Here are 3 tips (and some insight) to help you know how to prepare pre-approval.

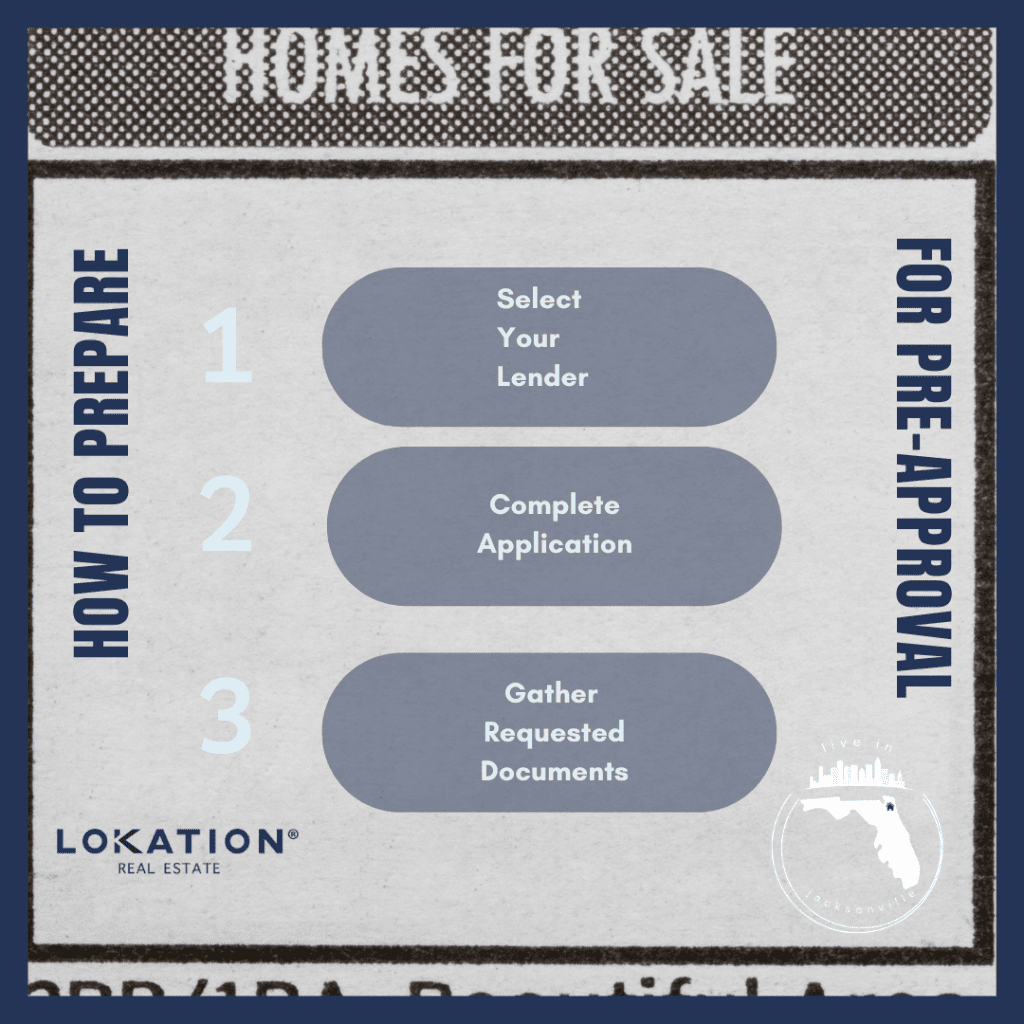

Select Your Lender

Whether you select a lender or real estate agent first is your choice (and a matter of preference). If you know a lender and don’t know a realtor – take this step first. Alternatively – with the opposite true – start with the agent (who likely has a list of suggested lenders to share). If you have neither in your contacts – proceed with the REALTOR first. Why? If there’s a chance you’ll consider new construction, lenders often have incentives available with preferred lenders. When selecting a lender – plan to talk with a few and ask questions. You want someone you find you’ll be able to work alongside. Going through the lending process is much like a financial physical (assets, debt, taxes and employment will be analyzed) and there’ll be regular dialog. Once you’ve select your lender you can proceed to the next step of completing the application.

Complete Application

With your lender selected, you’ll proceed to completing an application for mortgage. Filling out the paperwork is typically straightforward – however, completing the third step in advance of tackling the application may be in your best interest.

Gather Requested Documents to Prepare for Pre-Approval

In addition to the completed application, you’ll need personal identification, social security number, pay stubs, bank statements, tax returns, investment accounts (if applicable) and a list of debts. Your lender will run your credit and work with all the information you’ve supplied.

Know How to Prepare for Pre-approval

While all of this may seem time consuming and laborious – it is the front end of the mortgage process. The return for your time investment is (hopefully) a pre-approval letter. The letter will give you a firm idea of the amount of loan you’ll likely be eligible to take on. I intentionally use hedging words here are there are no guarantees in the mortgage process. The home needs to appraise, your financial profile needs to remain consistent and all information supplied needs to check out. With a pre-approval in hand and home shopping – you shouldn’t take on additional debt and keep your employment status quo. Major changes to your financial profile can jeopardize your loan application. Rest assured – as your loan application is not complete until you receive a clear to close notification – a contingency will be written into your offer regarding financing.

Financing a home can be stressful. Knowing how to prepare for pre-approval, pre-planning and selecting a lender of choice, will help you be well-prepared to enter the world of home shopping and buying. As always, if you have any questions on this process, please feel free to reach out to me and let’s schedule a call.